The World’s attention this week may be 12,500 km to the north – east but the dispute over the Panama canal has not gone away. Few infrastructure projects can match it for cost – perhaps 25,000 died when the French tried to build it before the US completed the job in 1914; or for value in that 13,000 ships carrying 250 million tons used it in 2025 instead of sailing 15,000 km around Cape Horn, representing 5% of World trade and earning the canal $5.7 billion; or, therefore, for political sensitivity.

I have acted as an expert witness in comparable, if lower profile, disputes where I have had my opinions tested on both possible financing terms in the event that the project had proceeded but also, and perhaps more importantly here, whether the allocation of risks and responsibilities was appropriate and the likelihood of each counterparty being able or willing to perform those responsibilities as originally intended. Key among these risks is, of course, the political one.

No resolution of the Panama dispute seems currently to be in sight but, based on my experience and viewing this dispute from afar, I can propose some tentative ones.

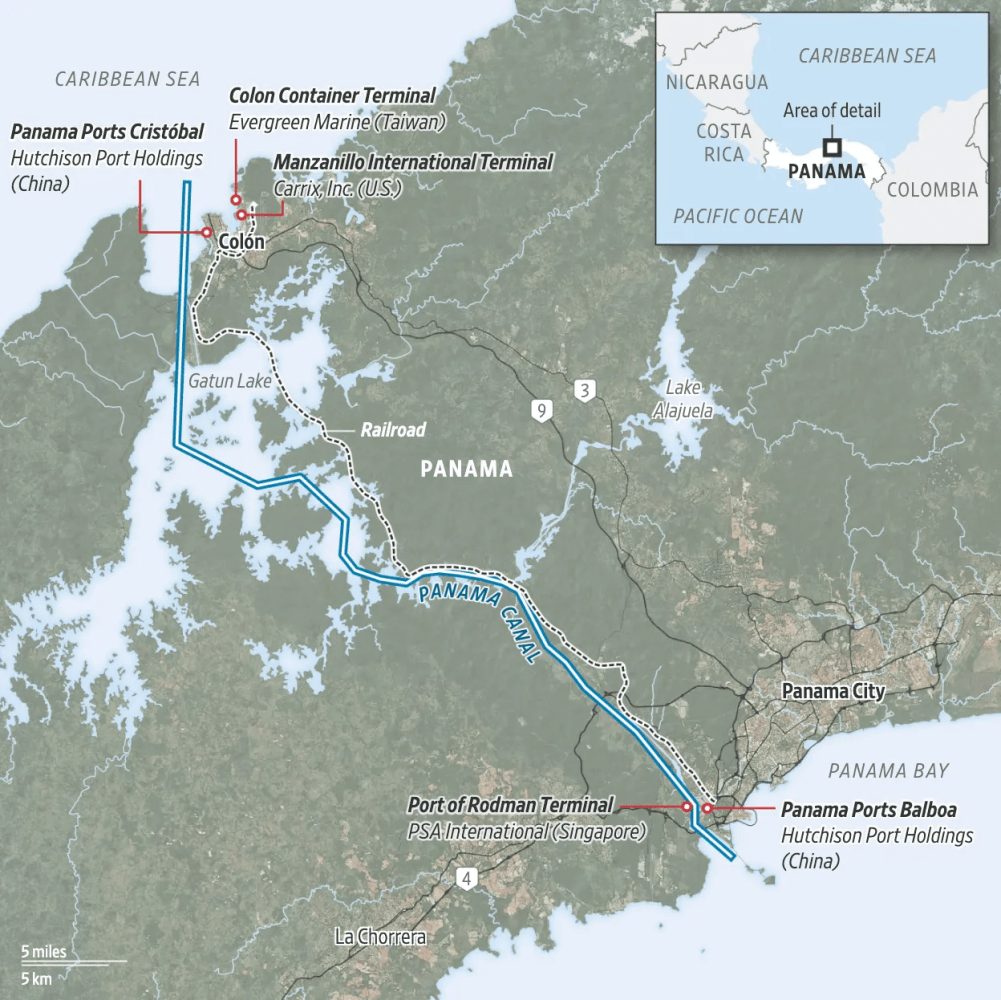

First, establish the facts. The canal itself is run by the autonomous Panama Canal Authority following a staged handover from the US completed in 1999 pursuant to the two Torijos – (Jimmy) Carter treaties of 1977 (foreshadowing the UK’s conundrum on the Chagos Islands today?). A $5.2 billion upgrade in 2007 – 2016 enabled it to accommodate Neo – Panamax ships but it is still vulnerable to drought impacting operation of its locks as it climbs 26 m through the mountains, most recently in 2024.

Separately, there are container ports at either end of the canal, two at Balboa on the Pacific coast and three at Cristóbal on the Caribbean coast. Since 1997, one at each end has been run by Panama Ports Co, owned 10% by the government and 90% by Hutchison Port Holdings, itself owned 80% by Hong Kong’s CK Hutchison Holdings and 20% by the Singapore government’s very quiet PSA International. These two ports have a 39% market share; Singapore’s PSA runs the other port at Balboa (market share 14%); Taiwan’s Evergreen Marine – whose Ever Given ran aground in the Suez canal five years ago blocking it for six days – (17%) and the US’ SSA Marine MIT (29%) run the other two at Cristóbal. The ports are mainly for trans – shipment enabling regional distribution. In addition to the container traffic, dry bulk, tankers, cruise ships and the military may – or may not – use the ports.

Separately, there are container ports at either end of the canal, two at Balboa on the Pacific coast and three at Cristóbal on the Caribbean coast. Since 1997, one at each end has been run by Panama Ports Co, owned 10% by the government and 90% by Hutchison Port Holdings, itself owned 80% by Hong Kong’s CK Hutchison Holdings and 20% by the Singapore government’s very quiet PSA International. These two ports have a 39% market share; Singapore’s PSA runs the other port at Balboa (market share 14%); Taiwan’s Evergreen Marine – whose Ever Given ran aground in the Suez canal five years ago blocking it for six days – (17%) and the US’ SSA Marine MIT (29%) run the other two at Cristóbal. The ports are mainly for trans – shipment enabling regional distribution. In addition to the container traffic, dry bulk, tankers, cruise ships and the military may – or may not – use the ports.

Panama and the US remain intertwined over the canal in that 59% of tonnage passing through the canal is American, much of it on its way from one US coast to the other; 16% is Chinese.

Next, identify the risks. Last year, the incoming second Trump administration rolled out its “Donroe doctrine” to exert more influence on what it considered its own backyard. It was particularly concerned about its geopolitical rivalry with China – and the two intersected at Hutchison and the Panama canal. Never mind that Hutchison was a listed company, not the Chinese Communist Party (although no doubt mindful of the latter’s position). Never mind that Hutchison didn’t run the canal. Never mind that there are competing ports at both ends of the canal and that the only ways to compete with a neighbour are i) faster turnaround ii) drop the price iii) establish global alliances so as to create captive customers iv) don’t compete i.e. establish a cartel. Plenty of players could inflict self – harm and block the canal by scuttling a ship, dropping a container overboard … or sending in the military. Nonetheless, the optics do matter.

Back in in 2017 during Trump 1, Panama had switched its interpretation of One China from Taiwan to the PRC and was the first country in Latin America to sign an MoU re the Belt and Road Initiative. However, pressure from Trump 2 was mounting and, perhaps sensing an opportunity to offload low yielding assets, in March last year Hutchison agreed to sell its portfolio of 43 ports across 23 countries, including PPC and retaining only those in Shenzhen and HK which are held in a separate trust. The buyer was a consortium led by the US’ Blackrock which had just bought Global Infrastructure Partners and Swiss / Italian MSC. The price looked pretty fancy at $23 billion. Blackrock would control the two Panama ports and MSC the other 41.

Beijing was not amused. It was just as sensitive as was the US to who controlled the canal / ports. It wanted the deal to be subjected to its merger review process even though none of the ports were in China; and for its State Owned Enterprise COSCO to be involved.

Meanwhile in Panama, various lawsuits had been rumbling along since 2021 (There is always scope for disagreement in a concession usually surrounding how much of the proceeds of a fantastically valuable asset accrue to the host and how much to the operator and would one side like to change this?) but not sufficiently serious to disrupt the cash cow. An audit in 2025 “found irregularities”. Then, coincidentally or otherwise, in January, the Supreme Court suddenly ruled that, when the concession was extended for 25 years in 2021, it had been done “unconstitutionally” in that it created a de facto monopoly. (The canal has its own Title XIV in the country’s constitution.) Last week the Panama Maritime Authority took back control of the ports, appointing APM Terminals, owned by Danish AP Møller-Maersk (no connection to Greenland …), to run Balboa and Terminal Investment Ltd, owned by the same MSC, to run Cristóbal until a new concession can be awarded within 18 months.

Hutchison has taken the government to arbitration at the ICC.

At the same time, Panama chose to not renew the MoU with Beijing, cutting itself off from potential PRC funding for future infrastructure projects.

This fight will be won and lost at the political level, of course, but it will be informed by the commercial position beneath. Consider the implications.

- Most governments Worldwide have powers of eminent domain i.e. they are entitled to expropriate an asset – if appropriate compensation is paid. However, President José Raúl Mulino made no mention of compensation when issuing his “occupation decree” which he described as “an exceptional legal tool”. The legal argument then moves on to how much should that compensation be? (There are twenty years still to run on the concession.)

- The concession entitles the government to terminate for public interest or national necessity and pay compensation accordingly.

- It is also entitled to terminate the concession for major breach such as failure to make the agreed investments. Did Hutchison breach the concession by not performing somehow? It seems unlikely when cure periods are provided for.

- Was the concession unconstitutional from the outset? Twenty nine years later? The original concession was enshrined in Law No.5 of 1997 and the extension in 2021 was also passed by the National Assembly, no less. Surely, Hutchison would have been entitled to rely on this. Nor does the monopoly argument look convincing when there is competition at both ends of the canal.

In conclusion, when viewed from afar, I can see the following tentative solution:

- Terminate Hutchison in accordance with the concession i.e. with full compensation.

- Auction the two port concessions separately to parties not already there. So, not the US (SSA Marine is a private company not owned, but no doubt influenced, by its government too). No one would be allowed to win both. China would be invited – Hutchison may have battle fatigue but COSCO, China Merchants et al would be interested. As would Dubai’s DP World.

- Hutchison is free to sell the other 41 ports to Blackrock / MSC or indeed anyone else at an adjusted price.

Cue howls of outrage from both sides? Assuming a Chinese player wins one of the new concessions, there is a balance of influence, but not control, between the US and China. As with all good compromises, both would be equally unhappy. The alternative is Panama reverting to being a vassal state of the US.