Deserved congrats to Singapore Inc for this week’s trifecta of conferences namely Infrastructure Asia’s biennial forum, the World Cities Summit and The Asset’s 11th Sustainable Infrastructure Finance Summit, all of which led – not just hosted – the necessary conversations about how to finance the region’s enormous needs on a sustainable basis.

Behind the style, however, blockages to deal flow persist and the players largely responsible for the unblocking weren’t there.

See Andrew’s support of The Asset at 4.38.

This is because it is host government officials, often the least experienced and least paid players in the piece, to whom fall the most difficult decisions when developing a project, be it designing the route of a road, judging future demand, securing land / clearing it of its occupants or designing the regulatory and legal regimes within which the private sector can then develop projects.

This is in the context of Asia comprising a huge variety of countries in terms of size (Indonesia makes up 40% of ASEAN ‘s population on its own): organizational clarity (still in Indonesia, how does Danantara sit in relation to its SOEs, the MOF, the Coordinating Ministry for Economic Affairs, Bappenas, the IIGF, SMI, probably others?); openness to private sector or foreign investors (contrast the Philippines); availability of deep – pocketed sponsors able to manage political risk (again, the Philippines), even religion / culture (Malaysia has access to Islamic finance).

Thus, the much – needed Multilateral Development Banks could be more impactful by i) lending on a more outcome basis i.e. with strings attached such that each drawdown on a sovereign loan is conditional on the host government doing something specific to make investments easier; ii) taking more first – loss risk on individual projects given that the market rarely needs just another commercial lender iii) structuring guarantees against specific risks especially in the revenue line and iv) by paying for external advice to host governments on more macro issues such as how to structure, allocate and recycle central government support for sub – sovereigns which are rarely rated or bankable on a standalone basis. Examples include SOEs, municipalities (important for water, the circular economy, etc.) and especially cities looking for some autonomy. But little of this is being discussed. Logie Group stands ready to advise on how to make all this happen!

Assorted further points:

In two full days of discussion, there was no mention of China’s Belt and Road Initiative which, after several years of irrational exuberance (potentially good for Logie Group’s dispute resolution business), financed a still chunky US$8.8 billion in Q1 in non – financial ODI to B & R partner countries. Any host government should be playing off one contender against the others, be it in terms of build quality, allocation of risk and contract rigour, resulting political influence or cost. Again, advice is needed.

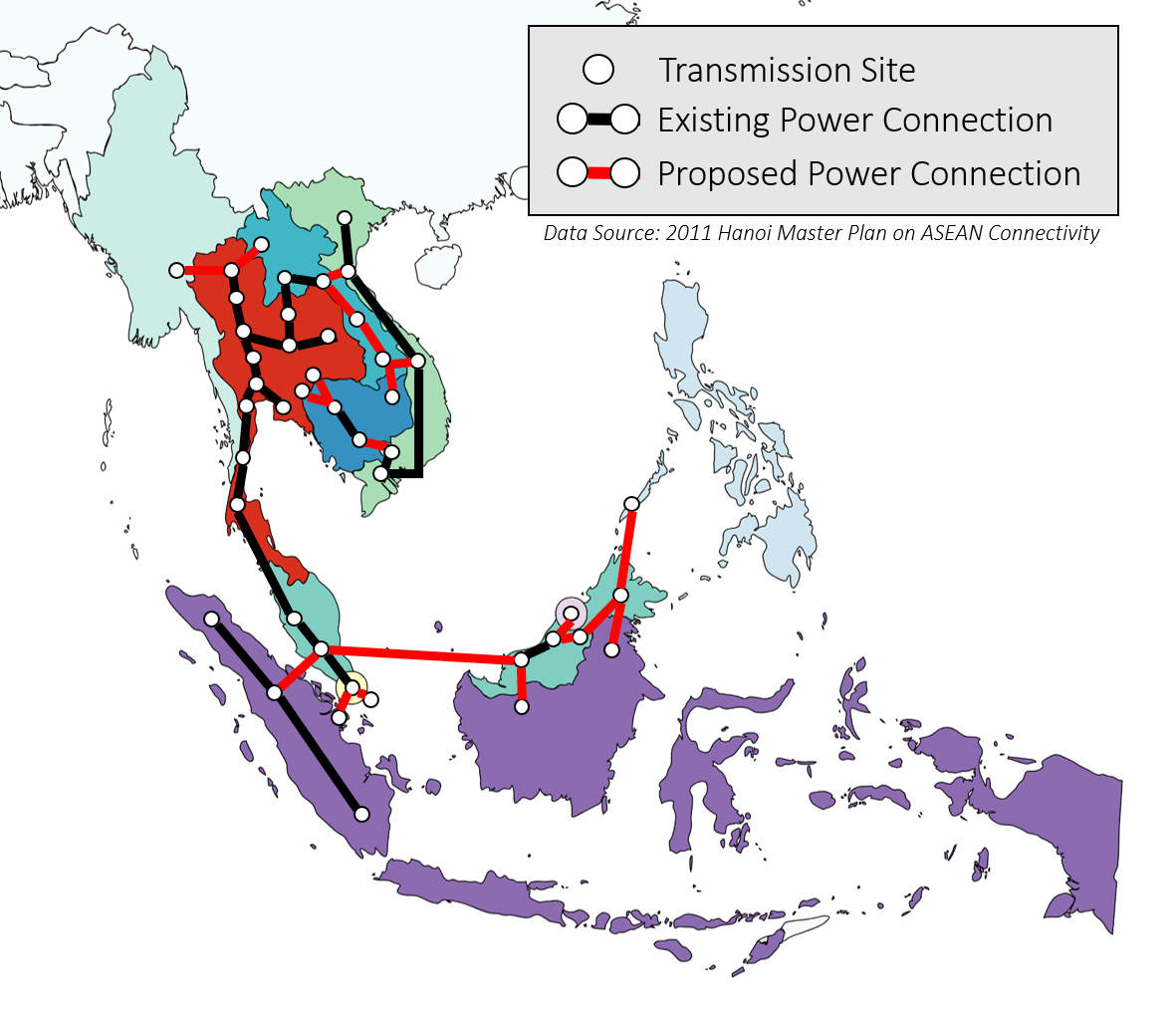

The ASEAN power grid is being promoted again. Connectivity / mutual dependence carries some political benefit, as in the EU; by all means, generate power where it is cheap and where it is still worthwhile to transmit it to where needed; but why, for example, connect Palawan to Sabah when you can spend the money generating locally?

The ASEAN power grid is being promoted again. Connectivity / mutual dependence carries some political benefit, as in the EU; by all means, generate power where it is cheap and where it is still worthwhile to transmit it to where needed; but why, for example, connect Palawan to Sabah when you can spend the money generating locally?

Surely, it is better to develop local bits of the grid where justified such as the several deals where Laos sells hydro to Thailand and is now selling wind power to Vietnam (the 600MW Monsoon project started up last year). Meanwhile, archipelagic countries such as the Philippines and Indonesia can nowadays substitute diesel on remote islands with wind / solar plus batteries and not need a grid at all.

There has been less talk recently about Energy Transition Mechanisms whereby coal – fired plants are closed down and replaced with renewables, with the Cirebon 1 IPP in Indonesia as the leading example. But closing down an operational asset incurs a significant opportunity cost and who was going to pay for this? At AIF, Vice Minister Rachmat Kaimuddin reiterated that it wouldn’t be Indonesia when it needed all the power that it could get.

There was much talk about the latest industry sector, namely data centres. The issue which wasn’t discussed here is the same as that with Public Private Partnerships where hospitals, schools, etc. are made available to governments. The cost of debt issued by the project proponent is inevitably higher than the sovereign / hyperscaler would pay so, in return for this, what risks are in reality being offloaded to the project proponent?

Small deal size remains a problem, especially for renewables, in that they yield what one speaker characterised as low ROE as in Return On Effort. Back in 2014, Andrew was involved in SAEMS’ sale of its Sri Lankan hydro portfolio which featured consistent PPAs with Ceylon Electricity Board. But such deals are rare.

Liquidity is also an issue. Clifford Capital has led two securitisations of project finance loans enabling the sellers to free up capital for reinvestment into the more development end of the risk profile. But again, such deals are rare.

The above points expand on the fruitful discussions that took place across all three events.

Essentially, just as in war (to invoke a contemporary example) where you should not assume that your opponent thinks as you do, in investing you should not assume that your counterparty has the same appetite, ability or commitment as you do. So, as usual, you should take advice – by now, you should know from whom!

(Meanwhile, over the water, the Scots are managing expectations and the Dutch are skipping their medication at the World Cup …)