It’s a question that is unlikely to pop up in your local pub quiz: what do Tammy Wynette and Miguel de Cervantes have in common? Especially as the answer lies in Vietnam.

Tammy, of course. advised ladies to Stand by their Man back in 1968 (before 68% of today’s potential listeners were even born). Even older advice came in two instalments in 1605 then 1615 when Miguel’s Don Quixote shot to fame for, amongst other matters, tilting at windmills (Bonus question: name any other of his works).

Tammy, of course. advised ladies to Stand by their Man back in 1968 (before 68% of today’s potential listeners were even born). Even older advice came in two instalments in 1605 then 1615 when Miguel’s Don Quixote shot to fame for, amongst other matters, tilting at windmills (Bonus question: name any other of his works).

In 1968 on the other side of the World, Vietnam had more pressing matters such as Agent Orange – no, not Donald Trump although this does involve what he refers to as windmills, namely wind turbines.

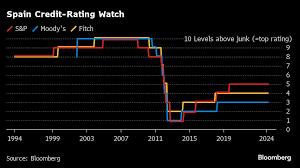

Fast forward to Miguel’s home country of Spain where, in 2014, the government decided to retroactively reduce the overly generous feed-in tariffs for mostly wind projects awarded in 2007 – 2012. Royal Decree 413 / 2014 replaced the previous system with a new one based on a “reasonable return” for investors new and old alike. Cue multiple arbitrations under the EU’s Energy Charter Treaty (ECT) and elsewhere, less appetite from investors for future projects, higher interest rates and more. All in all, as Spain discovered, sovereign default is generally a bad idea.

Back to Vietnam, 87% of the population was born after 1968 and they have recovered astonishingly from decades of war, epitomised by how bomb craters have been repurposed as fish ponds (pictured). In the 40 years to 2024, GdP per head grew almost seven fold even whilst the population almost doubled. The communist – led government relaxed its grip to great effect but sometimes overly so in that, like Spain, it also has form in not supporting its State Owned Enterprises. In 2010, the government allowed its SOE Vinashin, once the fifth biggest shipbuilder in the World, to default on a $600 million syndicated loan facility citing, of all things, bad behaviour by one of its own people. It took three years until the faraway High Court of England sanctioned a Scheme of Arrangement to share the pain via, inter alia, extended loan tenors, haircuts and an interest rate of only 1% but with a comfort letter replaced by an explicit MOF guarantee.

SOEs can, of course, act in the market as entities separate from the government that owns them. Counterparties’ willingness to transact with an SOE depends on the SOE’s standalone reliability as well as the actual and perceived support from its government. Thus, Thailand’s electricity SOE, EGAT, is a well run monopoly and creditworthy in its own right so does not need further government support. It is rated BBB+ by Standard and Poor, the same as the sovereign. Indonesia’s equivalent, PLN, benefits from having a public service obligation and the requirement under the Constitution that the MOF reimburse it for whatever the result. The market thus views PLN’s 30 year paper as effectively sovereign risk plus a little bit extra return. PLN is rated BBB by Standard and Poor, again the same as its sovereign. These levels of trust take years of good behaviour to build up.

Despite commendable progress recently, Vietnam hasn’t yet earned these levels of trust. Worse, the government now wants to repeat Spain’s mistake and reduce its support for the 20 – year Power Purchase Agreements signed since 2017 by its SOE Electricity Vietnam. The FT reports that 173 foreign and domestically sponsored solar and wind projects, aggregate cost $13 billion, would be involved. Even EVN considers this a bad idea as revealed in two letters to its boss, the Ministry of Industry & Trade, which have recently come to light.

Logie Group agrees with EVN. Andrew has advised on central government support for SOEs and other sub-sovereigns in countries such as Indonesia and India. He acted as an expert witness in a power dispute between the government / its SOE Electricite du Cambodge and a US investor in neighbouring Cambodia. His advice to the MOF in Vietnam, when it comes to windmills or indeed anything else, is that, absent bad behaviour by the counterparty, defaulting on commercial contracts which have been willingly and knowingly entered into has wide ranging consequences not just for the transaction concerned but also for the market’s view of its reliability going forward. So, Stand By Your Man.